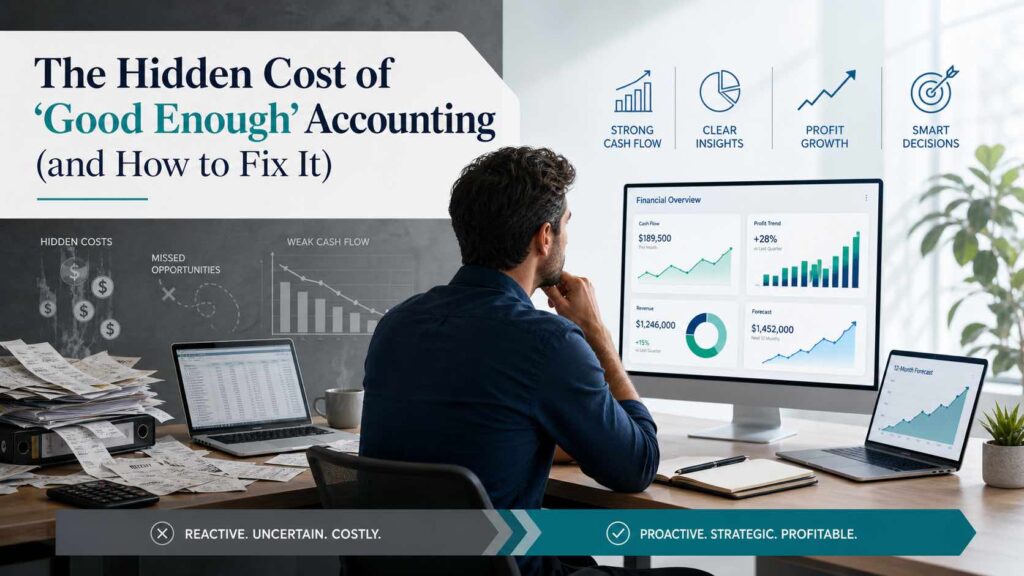

The Hidden Cost of “Good Enough” Accounting (and How to Fix It)

For many business owners, accounting falls into the “good enough” category. The books are updated (mostly), taxes get filed on time, and nothing seems obviously broken. On the surface, that feels like success.

But here’s the problem: “good enough” accounting is often quietly expensive. Not in obvious ways like penalties or missed filings—but in lost opportunities, poor decisions, and unseen inefficiencies that compound over time.

Let’s break down what “good enough” is really costing you—and how to fix it.

What “Good Enough” Accounting Looks Like

If any of these sound familiar, you’re not alone:

- Your books are updated monthly (or quarterly), but not in real time

- You rely on your accountant mainly during tax season

- Financial reports are generated—but rarely used to guide decisions

- You’re unsure how much profit you’re actually taking home

- Cash flow feels unpredictable, even when revenue is strong

Nothing here is catastrophic. But that’s exactly why it’s dangerous.

The Hidden Costs You’re Probably Paying

1. Missed Tax Savings

Basic accounting focuses on compliance—filing accurate returns. Strategic accounting focuses on minimizing your tax liability throughout the year.

Without proactive planning, you could be:

- Missing deductions

- Delaying entity optimization (like S-Corp elections)

- Overpaying in estimated taxes

Over time, this can mean thousands—or tens of thousands—of dollars left on the table.

2. Poor Decision-Making

When your financials aren’t timely or clear, decisions get made on instinct instead of data.

That can lead to:

- Hiring too early (or too late)

- Overspending during high-revenue months

- Underinvesting in growth opportunities

Good accounting should act like a decision-making system, not just a record-keeping tool.

3. Cash Flow Surprises

Revenue doesn’t equal cash. And “good enough” accounting often fails to give you a clear picture of what’s actually available.

This is how businesses end up:

- Profitable on paper but short on cash

- Scrambling to cover expenses

- Hesitating on growth because of uncertainty

4. Lack of Financial Visibility

If you can’t quickly answer questions like:

- “What’s my most profitable service?”

- “Where am I overspending?”

- “How much can I safely reinvest?”

…then your accounting system isn’t working for you—it’s just documenting the past.

5. Slower Growth

Perhaps the biggest hidden cost is missed momentum.

Businesses with strong financial systems:

- Scale faster

- Take smarter risks

- Adapt more quickly to market changes

“Good enough” accounting keeps you stable. But it rarely helps you grow.

How to Fix It: Moving From Reactive to Strategic

The goal isn’t just cleaner books—it’s better financial control and smarter decisions.

1. Shift to Proactive Accounting

Instead of looking backward, your accounting should help you look forward.

That means:

- Regular financial reviews (monthly, not yearly)

- Forecasting future revenue and expenses

- Planning for taxes before year-end

2. Build a Financial Dashboard

You don’t need 20 reports—you need the right 5–7 metrics, such as:

- Cash flow

- Profit margins

- Revenue by service or product

- Operating expenses as a percentage of revenue

This turns your numbers into actionable insights.

3. Integrate Tax Strategy Year-Round

Tax planning shouldn’t start in March or April. It should be ongoing.

A strategic approach includes:

- Quarterly check-ins

- Adjusting estimates based on performance

- Identifying opportunities before they expire

4. Upgrade Your Systems (and Support)

At a certain point, DIY or bare-minimum accounting breaks down.

Upgrading might mean:

- Better accounting software and integrations

- Automated workflows

- Working with an advisor—not just a preparer

5. Treat Accounting as a Growth Tool

The most successful business owners don’t see accounting as a requirement—they see it as a competitive advantage.

When your financials are clear, current, and strategic, you can:

- Move faster

- Spend smarter

- Grow with confidence

Final Thought

“Good enough” accounting feels safe. But it often comes at a hidden cost—one that shows up slowly in missed opportunities, unnecessary taxes, and stalled growth.

The fix isn’t complicated. It’s about shifting from reactive compliance to proactive strategy.

Because in business, the difference between “good enough” and optimized isn’t small—it’s often the difference between staying busy and building real wealth.

If you’re ready to move beyond “good enough,” working with a proactive advisor like STR CPA Firm can help turn your financials into a tool for smarter decisions and long-term success.

{kind=link}

{kind=link}

{kind=link}